Market outlook: What’s Ahead for Canola?

Compared to the large swings of the past few years, canola prices so far in 2017-18 have remained fairly stable. (This was written in mid January.) The average Western Canadian bid has moved from a harvest low of $455 per tonne ($10.30 per bushel) to an early November high of $495 per tonne ($11.20 per bushel) and is now somewhere about halfway between. A move of less than a dollar per bushel over the past six months isn’t much. But that’s already history. The question is what to expect for the rest of 2017-18 and into 2018-19?

Soybeans: Watching weather in South America

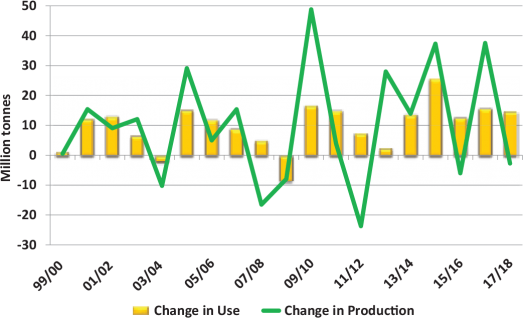

Soybeans are the overriding market influence for oilseeds. From the big picture perspective, global consumption of soybeans has been increasing at an average of 16 million tonnes per year over the last five years. That’s the same growth rate as the average increase in production, but there’s a whole lot more variability in year-to-year production, and that adds volatility to the market. (See graph 1.)

Global soybean consumption for 2017-18 is expected to rise another 15 million tonnes while production is forecast to actually slip by three million tonnes. Even so, overproduction in 2016-17 meant a large increase in the carry-in for 2017-18, so supplies still aren’t shrinking.

We’re already a few months into the 2017-18 soybean marketing year, but outcomes in South America, comprising half the global crop, still aren’t decided. Weather in Brazil and Argentina has become the dominant market factor. As of mid-January, the Brazilian crop was looking positive, although there are concerns about excess moisture causing diseases and harvest delays. In contrast, Argentina had been very dry but has since picked up some more moisture.

South American crop outcomes will be the largest factors for the rest of 2017-18, especially as they will determine the level of U.S. soybean exports. So far, U.S. exporters have been moving fewer soybeans than last year, raising the potential for larger U.S. ending stocks. That’s not helpful for prices. This slower export pace has also triggered commodity funds to build a large short position in soybeans, which has been pressuring futures.

Global soybean consumption for 2017-18 is expected to rise another 15 million tonnes while production is forecast to actually slip by three million tonnes.

Graph 1. Change in soybean use and production

Strong demand for canola

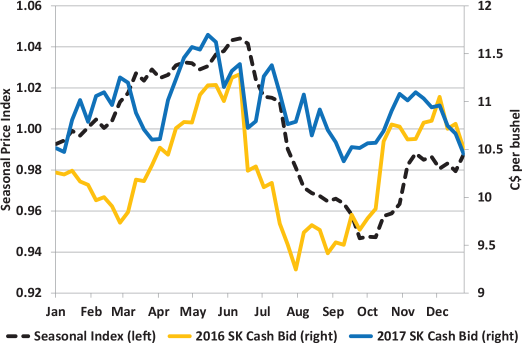

Canola has been feeling that spillover pressure from the soybean market, causing prices to decline late in 2017. Even though there’s not a whole lot of fresh news for canola as we roll into the beginning of 2018, there is some room for optimism based on seasonal tendencies. Typically, canola cash prices tend to move higher until mid-June with help from futures but also narrower basis levels. Early in both 2016 and 2017, there were a couple of dips but overall, prices followed those seasonal patterns fairly closely. (See Graph 2.)

Even though Canada’s 2017 canola crop was a new record, there’s no reason to think the same seasonal tendencies won’t show up in early 2018. Canola crushing so far in 2017-18 has been following last year’s record pace and canola exports (as of mid-January) are running at a new record. While a lot of the focus has been on Chinese demand, exports to Japan and Mexico have also been well ahead of last year. That solid usage means a steady pull of canola through the elevator system and continued price support.

Graph 2. Seasonal price index – Canola

For more canola market stats, go to canolacouncil.org and look under the “Markets & Stats” heading.

Seeded acres for 2018-19

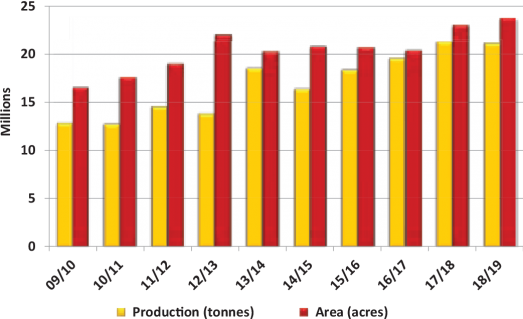

The look ahead to 2018-19 starts with ideas about this spring’s canola and soybean seeded area. Because of the discouraging market situation for pulses, most observers expect Canadian canola acreage to increase. We’re certainly in that camp. When we compare projected 2018 returns for canola versus other crops, canola comes out near the top. Disease concerns could limit the acreage increase, so we’re forecasting a modest three per cent gain this year. That still means another new record of 23.75 million acres. (See Graph 3.)

If the 2018 canola yield ends up close to the five-year average, Canadian production would be very close to the 2017 crop, leaving 2018-19 supplies essentially unchanged. On the consumption side, canola crush won’t change all that much as industry capacity stays the same. Exports will likely continue to expand as that’s been the consistent trend over the past five years. Based on all these assumptions, Canadian canola 2018-19 ending stocks could actually end up a little tighter than the current marketing year.

Graph 3. Canadian canola area and production

Global production

On its own, this Canadian outlook for 2018-19 should help support prices but developments in other countries for both soybeans and canola/rapeseed need watching. Those same market signals that will encourage Canadian canola acreage are also visible in other countries. Rapeseed is mainly a winter crop in Ukraine and the European Union and acreage already planted for the 2018 harvest is estimated to be steady or higher. Later this spring, plantings will likely be higher in Russia and Australia, two other key export competitors.

Despite this increase in seeded area, global supplies of canola/rapeseed won’t expand all that much (assuming average yields). This means the canola portion of the oilseed outlook isn’t going to become burdensome and that should be supportive for new-crop prices.

As always, soybeans will dominate next year’s oilseed outlook. Here in Canada, soybean performance in parts of the Prairies was less than stellar in 2017 and that could cause 2018 seeded area to plateau. But that’s hardly going to cause a ripple in the market.

Even if acreage of soybeans and canola is higher in 2018, yields also need to be average or better to maintain adequate supplies as there’s little “wiggle room” for crop problems in 2018-19.

The three dominant players in soybeans are the U.S., Brazil and Argentina, which together account for 80-85 per cent of global production. In the U.S., observers are already forecasting another small increase in 2018 soybean acreage as it seems to be penciling out a little more favourably than corn, causing acres to shift.

In South America, the 2017-18 crop is still out in the field so it’s far too soon to forecast next year’s acres. That said, Brazil has been steadily increasing acreage for years and there’s no reason to suspect that trend will change based on current market dynamics.

The main thing to keep in mind is that the world needs larger supplies of oilseeds every year, both for the oil and the meal. Production needs to keep expanding to meet that demand. Even if acreage of soybeans and canola is higher in 2018, yields also need to be average or better to maintain adequate supplies as there’s little “wiggle room” for crop problems in 2018-19.

This means (just like every year) the outlook is largely in the hands of the weatherman. And, like most years, there are already some concerns. In Western Canada, soil moisture is extremely low, especially in central Saskatchewan. Farmers in Ukraine are also worried as (through mid-January), their winter rapeseed crop has no real snow cover. While it’s too soon to draw any conclusions about the 2018-19 soybean crop, even the Argentine crop currently in the field faces challenges due to dry weather. These potential problems can still be resolved, of course, but they’re worth watching.

Based on assumptions of “normal weather,” the price outlook is relatively friendly, but despite all the economic analysis, weather still trumps all other factors in the outlook.