Vegetable oil and oilseeds outlook

Canola prices should be considered very attractive at $500-525 per tonne, especially after Western Canadian farmers produced a record crop. But how long can these high prices last? We all know it cannot be forever.

Current prices are supported mainly by delayed impacts of the 2015-16 severe drought in Southeast Asia that reduced palm oil production. Secondary factors are global tightness in rapeseed and canola, and recent flooding in Argentina that disrupted traders’ perspectives on soybean production in that country for 2017.

While we don’t know yet this year’s actual soybean production in Argentina, the drop in palm supply is real. And because palm oil is the biggest oil crop in the world, it has had an unprecedented impact on global vegetable oil prices. The ongoing tightness and relatively high prices of most vegetable oils in January-March 2017 are spilling over to canola and rapeseed. But that pendulum will swing back.

Over the next 12 to 15 months, the world will move away from tightness in the supply of oils and fats. This will start sometime in mid-2017, initiating a price decline that will accelerate. Under the lead of palm oil, world vegetable oil supplies will have a large increase in 2018. With “normal” weather, this should induce a considerable bearish trend in January to June 2018.

Palm oil

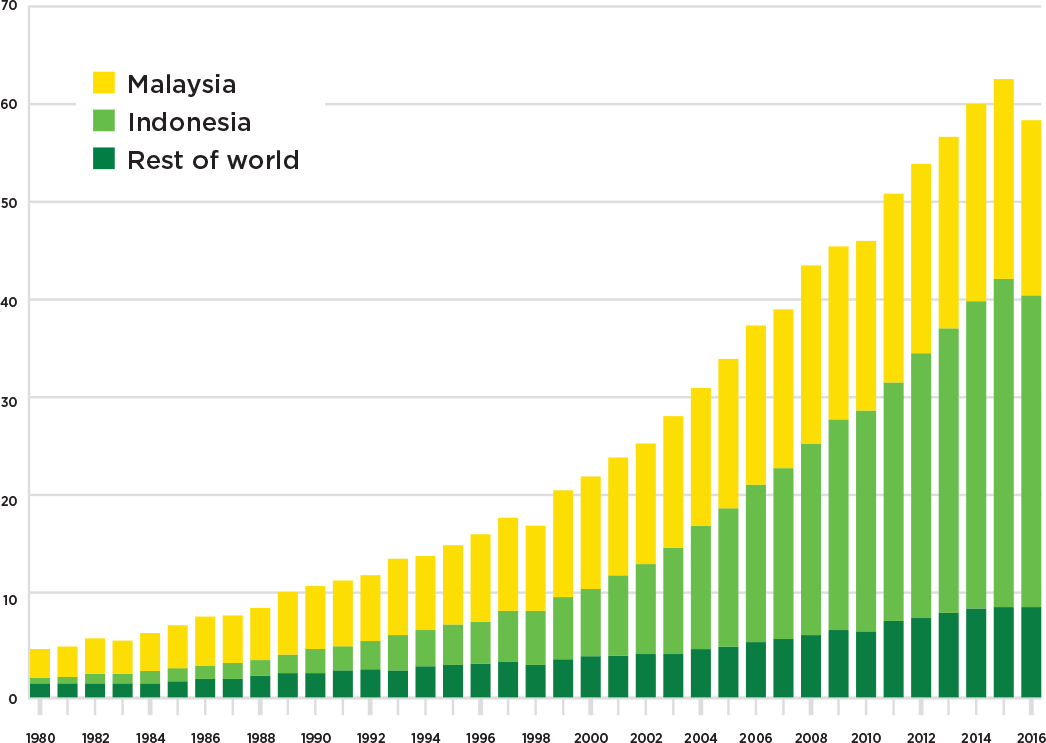

Palm oil is the biggest player in world vegetable oil markets. Oil palm plantations in Indonesia and Malaysia are the single biggest suppliers of vegetable oils and, despite the drought-induced drop in palm oil output in 2016, productivity continues to leap well ahead of second-place soybeans — even though both have seen fairly steep production increases over the past few decades.

Palm trees, once established, produce oil-rich fruit bunches all year long. Workers harvest the trees every two or three weeks, and well-managed plantations produce six to seven tonnes of oil per hectare per year. Palm trees react sensitively to disturbances, like drought, but the effects on actual production are shown with a time lag.

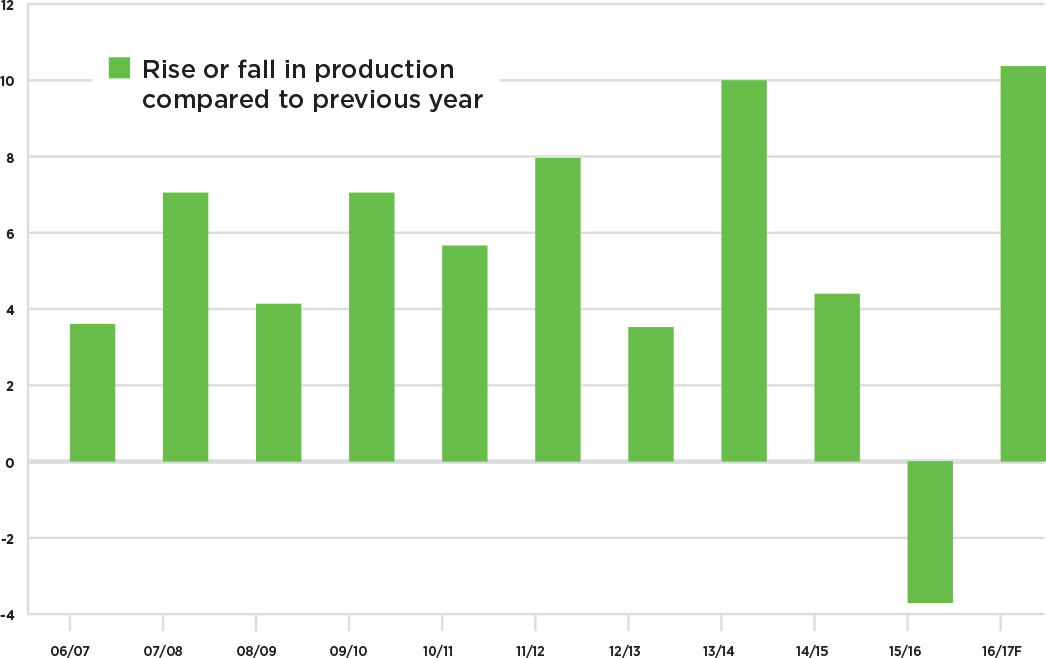

In 2015 and early 2016, Indonesia and Malaysia experienced one of the worst drought and heat conditions in the past 40 years. This created the biggest global production deficit ever experienced and a corresponding reduction of stocks. In fact, a year-on-year decline in palm oil is unusual. Since the 1970s, world production of palm oil doubled every 10 years. The steep drop in 2016 by a combined 4.2 million tonnes for Indonesia and Malaysia significantly reduced supplies and turned out to be the biggest price mover during most of last year. Production will start coming back in 2017, but the full recovery in palm oil yields and production will happen only in 2018. When stocks recover, prices will decline – probably sharply.

“I like to start a bit more general, checking results in my season zone, and then looking into the results in my province and finally my region, weighing out the results at each level.”

Soybeans

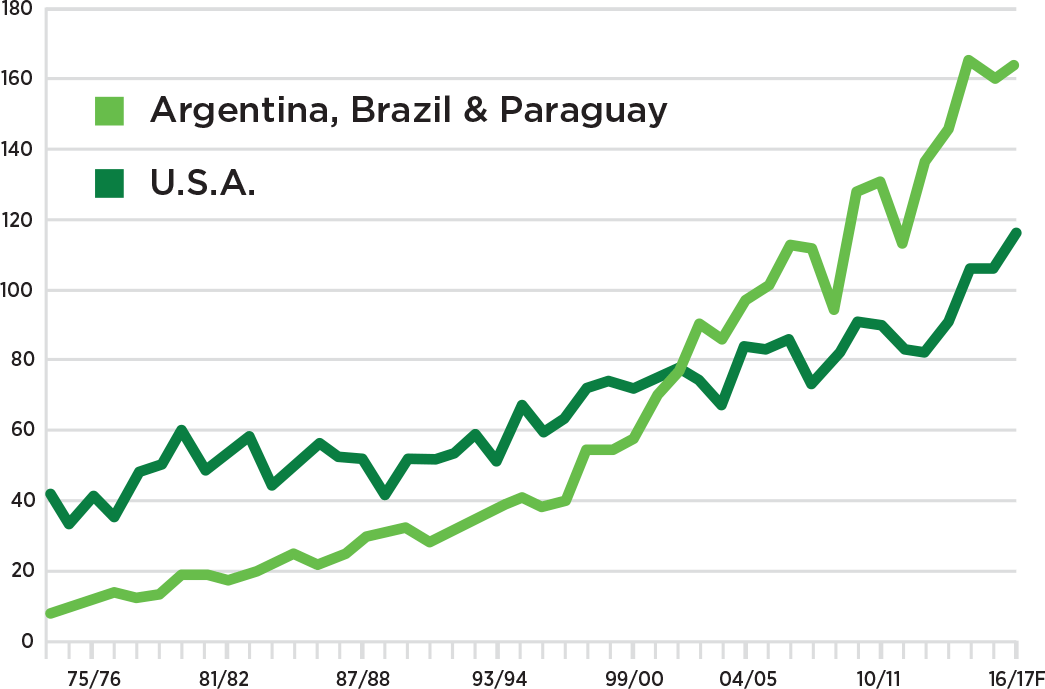

The U.S. registered both record soybean yields and production in 2016. Over the past four years, U.S. production jumped by 34 million tonnes. In my opinion, such a growth in production is unlikely to continue as it would be unusual to see another increase in U.S. soybean yields in 2017. South America will also see slower increases in soybean production, despite a record crop in Brazil. Argentine soybean output will decline in 2017 due to another reduction in the area and damage from heavy flooding in January. Also, the growth in Brazilian acreage is slowing down.

The world is becoming increasingly dependent on soybeans, but an oil supply tightness cannot be solved by crushing more soybeans without creating a surplus in meal. Soybeans are 79 per cent meal. A meal surplus is already influencing prices. In 2016-17, meal prices have come under pressure as price concessions have to be made to stimulate demand. Oil has to finance a larger share of the crush value. A rising oil share is an advantage for high-oil crops like canola and contributed to the price increase in early 2017. However, Canadian crushers of canola might not crush more canola if they can’t move the meal.

Export Logistics

Canadian canola exports represent 72 per cent of the total global canola and rapeseed exports. The share could be higher. The world, especially Asia, needs more canola oil and meal, but logistics are not in place in Canada to deliver it. Without capacity to export more canola oil and meal through Vancouver, the Canadian crush volume could be capped and Canadian canola growers will lose the opportunity to make more money. This is a challenge growers and the industry have to take on. To take advantage of the growing world market, Canada needs to boost inland transportation, storage and export capacities for canola, canola oil and meal as well as for other oilseeds and grains in a timely manner.

Global Canola and Rapeseed Production Dropping

Vegetable oil demand continues to increase, but farmers are running away from canola and rapeseed in other parts of the world. Ukraine is shifting to sunflowers, giving up winter rapeseed after two or three years of heavy winter kill. Europe and China are also reducing production. In 2016-17, China has produced only about six million tonnes, no longer the 12 million tonnes or more that it used to. World production of rapeseed and canola is thus seen declining in 2016-17 for the fourth consecutive year. Farmers in Canada and Australia are benefitting and are expanding canola production and exports.

Biodiesel

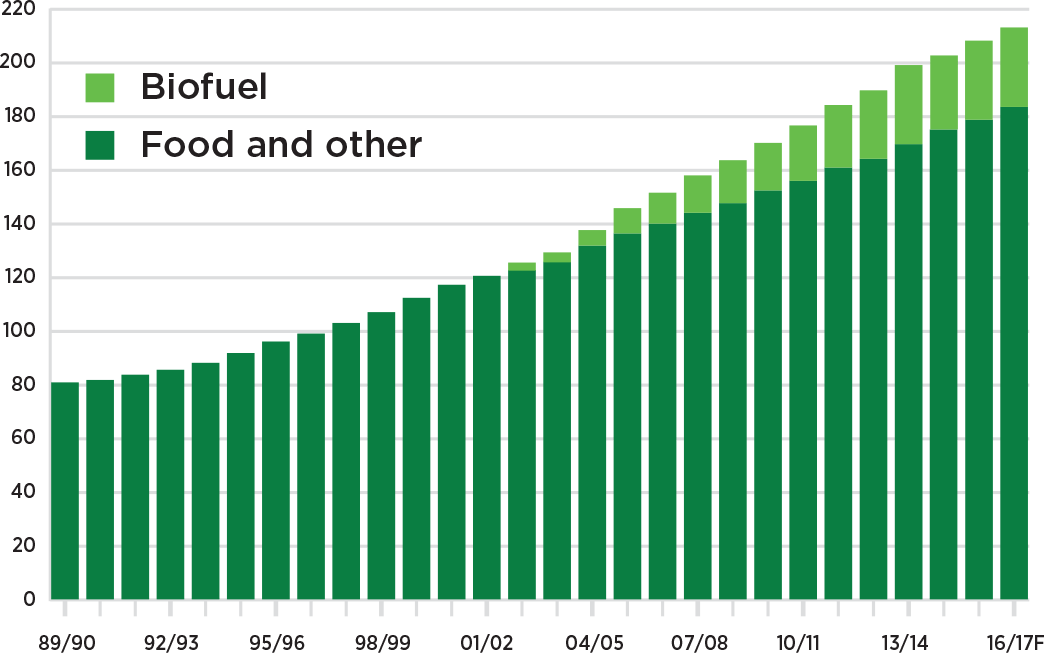

The European Union is considering a new biodiesel policy to stop using first-generation feedstock (like rapeseed oil, palm oil and soya oil) beyond 2020. It is proposed to allow only used recycled fats (say from food fryers) or other second- or third-generation feedstock. If passed, this policy would eliminate about 10 million tonnes of vegetable oil consumption in a short period of time, creating shockwaves across world vegetable oil markets.

The resulting bearish price trend in Europe would spill over to the world market and would have the greatest effect on marginal producers, particularly those in China and India, who can barely cover production costs at current prices. Farmers in Canada and other countries would be affected, too. Production would decline in the high-cost regions and increasingly shift to the most productive regions, primarily to Southeast Asian palm oil and the South American soybean growing regions, thus threatening further acreage expansion in environmentally sensitive regions.

I think at the end of the day the E.U. will not implement such a policy. It may instead slightly reduce or just freeze biodiesel production from first-generation feedstock.

Trade Between the U.S. and China

What would happen if the U.S. government increased import taxes on Chinese consumer products and China retaliates by raising the import tax on U.S. soybeans? Will it reduce soybean production in the U.S. and reduce soybean trade? I don’t think so. With domestic production insufficient, Chinese soybean import needs will continue to grow. Thus, implementation of an import tax on U.S. soybeans would just change trade flows. China would buy more from South America. In response, Europe and other Asian countries would buy more from the U.S.

At the end of the day, this would only make soybean imports more expensive for the Chinese, so I don’t think they will raise import taxes. Either way, it probably won’t affect Canadian canola much. But as China is becoming more and more dependent on oilseed imports, it may buy more canola from Canada and Australia anyway. Canada should improve logistics to be able to satisfy this increased foreign demand.

— Thomas Mielke is the editor and executive director of ISTA Mielke GmbH (Oil World Publications) in Hamburg, Germany. The company website is www.oilworld.de. He presented this outlook at Ag Days in Brandon in January.